Dynamic Asset Allocation Portfolios

Disclaimer: No bank guarantee, may lose value.

Why the Dynamic Asset Allocation Portfolios Are Superior to Any Fund Menu for Any 401k Plan

- It is a Universal phenomenon: Employers change 401(k) providers nearly every five years. And the number 1 reason ( just ahead of “poor service”) is the complaint echoed by their employees: “we’re just not making any money.”

- The Average 401(k) saver has earned LESS than 4% a year, in ANY five year period going back to 1990. Your fund menu may be a decent list. But employees SABOTAGE THEIR CHANCES BY FREQUENTLY MOVING THEIR ASSETS AROUND.

- Employees today are not actively monitored by a 401k Coach as to what changes they make intra-year. Those changes stem from emotional reactions to uncontrollable events, such as market volatility, politics, the economy, worries about potential war. Employee panic turns into “buying high and selling low.” Left unattended and not reversed back to their originally selected model will actualize a paper loss. This is what wrecks their plans for a sufficient retirement nest egg, forcing employees to make unpleasant decisions in the future that could have been avoided.

- Employees do not possess the tools for a self evaluation of their risk sensitivity Rs (their emotional assessment) and risk tolerance Rt (what maximum level of risk they should assume to achieve a desired savings balance) which will support a consistent quality of life after retirement--with their current savings balance. This disfunction, coupled with a lack of discipline and no monitoring by a professional 401k coach (again, no other firm does this) leads to most employees retiring with large deficit balances toward their savings target.

- Many plans have either too many mediocre fund options, or multiple fund options of the same type, thus creating employee confusion and indecision. 30% of plans have two or more fund options of the same investment type. Plans lose 2% of plan participation with each additional fund option beyond 10. Finally,

“target date” funds are the biggest cheaters, loading up on stocks in what should be the most conservative fund on the menu. If your 401k Committee selected target date funds, I’m sorry. There’s a better way.

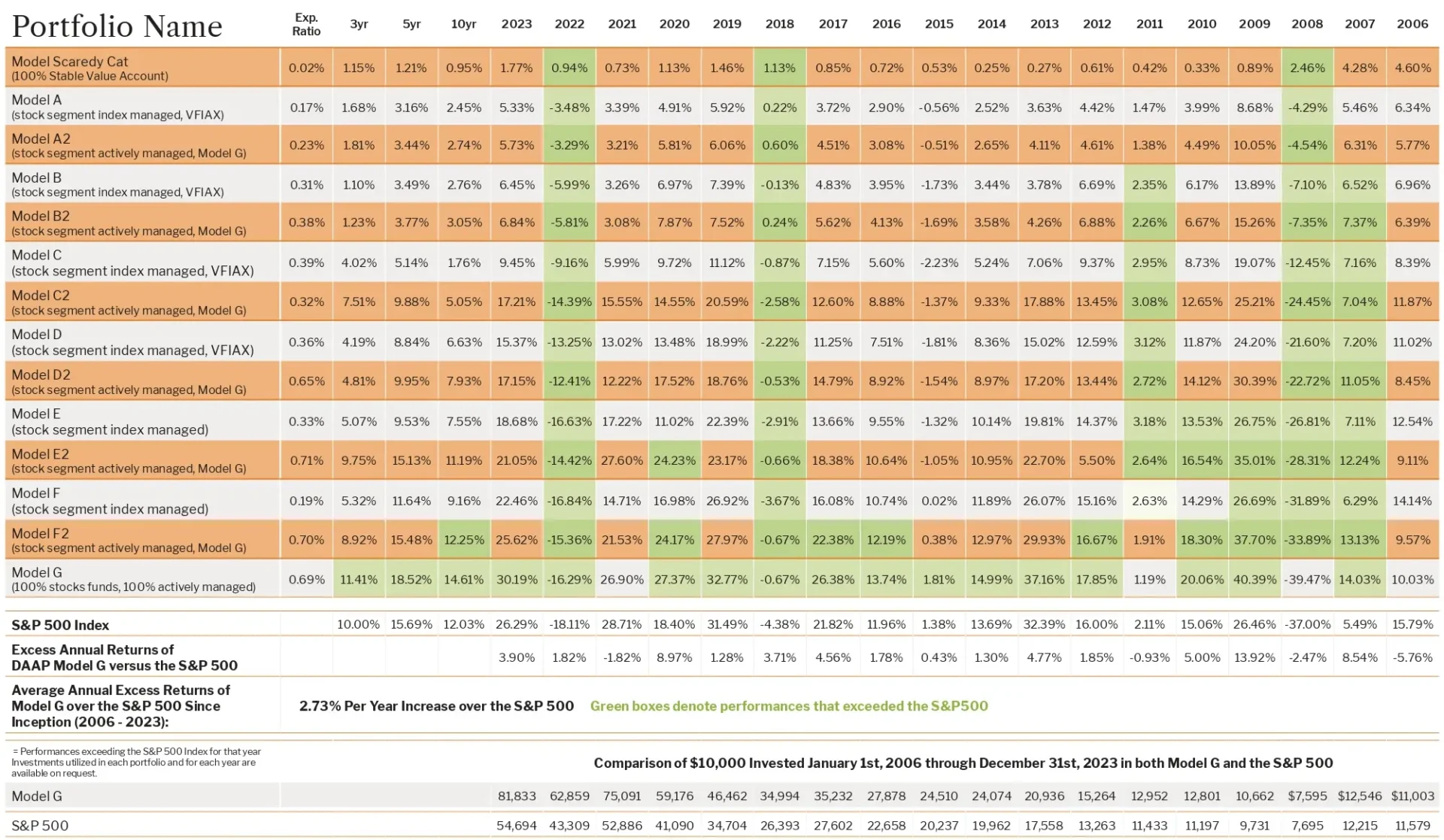

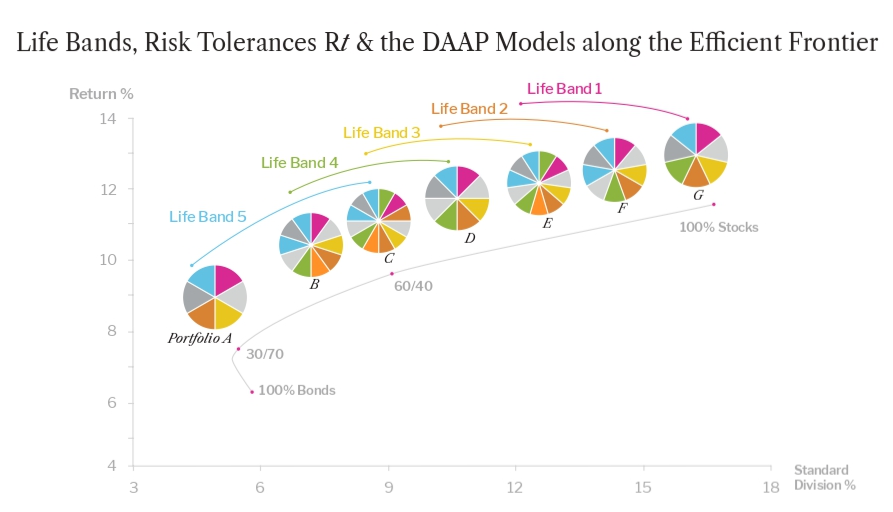

- The Dynamic Asset Allocation Portfolios are a series of Eight risk-based Models, from low volatility – low return, to high volatility – high return. The DAAP models mitigate the 5-year cycle of plan turnover, from one vendor to the next vendor.

- The DAAP Models attenuate the volatility experienced in Model G (the most aggressive yet most rewarding model) to Model A, using investment grade domestic bond fund holdings with their average maturity at 3.5 to 5 years–typically the least-volatile section of the yield curve.

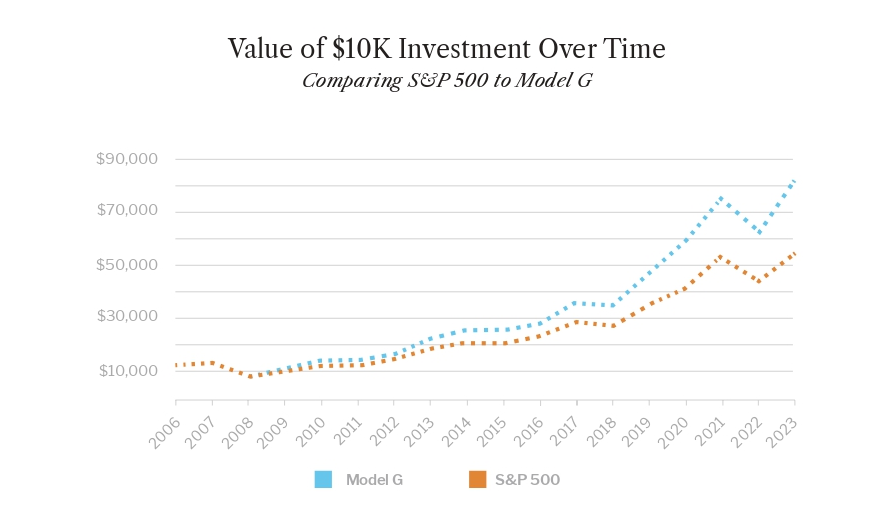

- Model G has beaten the S&P 500 Index 14 out of the last 18 years, with an average annual outperformance of the S&P 500 by 2.73%.

- Employees are monitored semi-annually and contacted by The Center for any changes they may have made to their deferral percentages or DAAP model switch, thus building a higher satisfaction level among the employees. It’s a feature of our 401k Coach® service. Employee contacts are even more frequent if

they enroll in our WellSpring Financial Wellness® program. We build a dossier on each employee, noting all calls and emails, the conversations and changes. - Our philosophy is to SAVE MORE – RISK LESS

- Our investment screening criteria, out of over 30,000 mutual funds and exchange-traded funds:

- Style and market capitalization purity, first. You learn quickly that most mutual funds cheat.

- Consistent outperformance in its style and market capscreened peer group, with the

- Lowest coefficient of correlation to each other – expenses breaking any ties.